| Version 22 (modified by , 16 years ago) (diff) |

|---|

Package QltvRespModel

Max-likelihood and bayesian estimation of qualitative response models.

Weighted Boolean Regresions

Abstract class

@WgtBoolReg

is the base to inherit weighted boolean regressions as logit or probit or any other,

given just the scalar distribution function  and the

corresponding density function

and the

corresponding density function  . In a weighted regression

each row of input data has a distinct weight in the likelihood function. For

example, it can be very usefull to handle with data extrated from an stratified

sample.

. In a weighted regression

each row of input data has a distinct weight in the likelihood function. For

example, it can be very usefull to handle with data extrated from an stratified

sample.

This class implements max-likelihood estimation by means of package NonLinGloOpt and bayesian simulation using BysSampler.

Let be

the regression input matrix

the regression input matrix

the vector of weights of each register

the vector of weights of each register

the regression output matrix

the regression output matrix

The hypotesis is that

![\pi_{i}=Pr\left[y_{i}=1\right] = F\left(X_{i}\beta\right)](../chrome/site/images/latex/838c94f04418fa55336d6713bf038357.png)

The likelihood function is then

and its logarithm

The gradient of the logarithm of the likelihood function will be

and the hessian is

User can and should define scalar truncated normal or uniform prior information and

bounds for all variables for which he/she has robust knowledge.

When  is infinite or unknown we will express a uniform

prior.

When

is infinite or unknown we will express a uniform

prior.

When  or unknown we will express that variable

has no lower bound.

When

or unknown we will express that variable

has no lower bound.

When  or unknown we will express that variable

has no upper bound.

or unknown we will express that variable

has no upper bound.

It's also allowed to give any set of constraining linear inequations if they

are compatible with lower and upper bounds

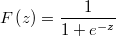

Weighted Logit Regression

Class @WgtLogit is an specialization of class @WgtBoolReg that handles with weighted logit regressions.

In this case we have that scalar distribution is the logistic one.

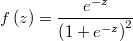

Scalar cumulant:

Scalar density:

Scalar density derivative:

Logarithm of likelihood:

Gradient:

Hessian:

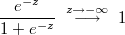

From the standpoint of arithmetic discrete numerical calculation must take into account that

For this reason we must carefully try to contain the exponential expressions.

In this case it will use the following asymptotic equalities

Weighted Probit Regression

Class @WgtProbit is an specialization of class @WgtBoolReg that handles with weighted probit regressions.

In this case we have that scalar distribution is the standard normal one.

Scalar cumulant:

Scalar density:

Scalar density derivative:

Logarithm of likelihood:

Gradient:

Hessian:

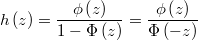

To avoid numerical problems will use the following equality

The function logarithm of complemetary error function

is implemented as gsl_sf_log_erfc that is available in TOL.

In the gradient it appears two times the Hazard function

decreases rapidly as  approaches

approaches  and asymptotes to

and asymptotes to

as approaches

as approaches

Hazard function is implemented as gsl_sf_hazard that is also available in TOL.